Africa's real estate markets entered 2026 in cautious recovery. Across the continent, the economic volatility of 2023 and 2024, driven by strengthening of the dollar against local currencies, sovereign debt stress, and post-pandemic fiscal tightening, had begun to ease. Growth forecasts from the IMF and World Bank were improving. Institutional investors were revisiting allocation conversations until the escalation of the Iran-Israel conflict interrupted that recovery.

Unlike other shocks that were primarily felt through exchange rates, the war is disrupting supply chains in the built sector resulting in increases in the cost of construction materials and energy that underpin both the delivery and operation of real estate assets across the continent. The extent of the impact of the war cannot be fully quantified yet, neither do we know when the war will end. Nonetheless, here are (just a few) of our thoughts on the direct consequences of the war on the market particularly from a transactions, construction and asset operations standpoint.

Before we dive in, here is some context on the war and why it matters for the African market.

On 13 June 2025, Israel launched a preemptive strike on Iran's nuclear facilities and military infrastructure, triggering sustained retaliatory exchanges and direct US military involvement that escalated through the first half of 2026. The strategic consequence relevant to African markets is the effective closure of the Strait of Hormuz — the passage through which approximately 20% of global oil trade and a significant share of containerised freight transits.

Although Africa has no direct role in the conflict, the closure of the Strait of Hormuz is feeding directly into African real estate costs. With roughly 70% of construction materials in Nigeria and many other African markets imported, the resulting disruption to global commodity supply chains, shipping costs, and refined petroleum prices has had an immediate and material impact on the cost of building and operating real estate across the continent.

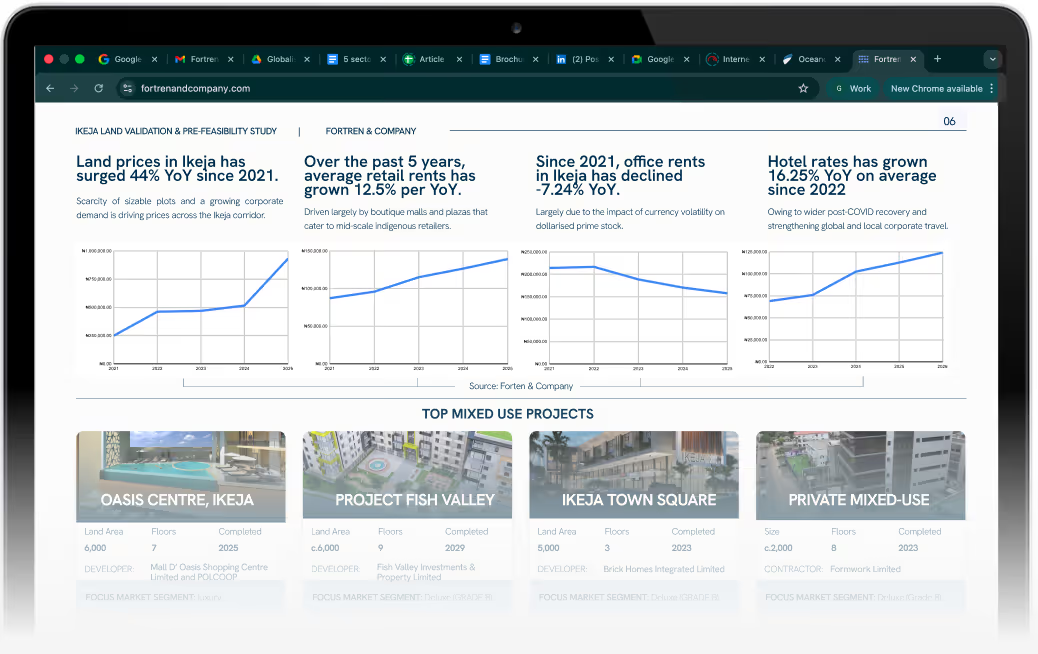

Construction costs in Nigeria rose 20% between December 2025 and May 2026.

One of the direct impacts we are seeing is an increase in the cost of building materials. In the past five (5) months, construction costs have risen by 20% in countries like Nigeria. While the impact has not yet reached the severity of the 2023 foreign exchange shock, Nigeria's limited tolerance for supply-side disruption means the effects are already material. Ongoing projects are struggling to reach completion, and conceptual ones are taking longer to mobilise to site.

Although the volatility has introduced cost-overruns to the market, the more consequential threat is the return of unpredictability and weakening investor confidence. Faced with sustained price volatility, contractors across Nigerian and West African markets are abandoning fixed-price contracts in favour of phase-by-phase pricing arrangements. While this structure protects contractor margins, it transfers cost risk squarely to developers, many of whom operate financing structures with insufficient flexibility to absorb it.

Transaction activity across African markets has slowed, with multilateral institutions revising down growth forecasts for the region in response to the uncertainty.

In markets where dollar-denominated assets dominate the prime segment, the conflict has added a geopolitical risk premium that is translating directly into pricing and deal velocity. In Nigeria, the slowdown is worsening an existing purchasing power crisis that predates the conflict.

The 2023 fiscal reforms by the present administration, although necessary over the long term, triggered an immediate contraction in real household incomes that suppressed transaction velocity. On Victoria Island, Ikoyi, Oniru, Banana Island, and the Eko Atlantic axis, rents have risen 15% to 35% as landlords hedge against further naira depreciation. Majority of developments that were sold off-plan in Lagos over the past two years cannot be delivered at the price and specification at which they were sold.

Developers managing this transparently are attempting renegotiation. Others have gone silent, or are value-engineering specifications downward to close the cost gap. Both responses are impacting investor confidence in an already-low-trust environment.

Conflict-driven increase in energy costs is making real estate assets more expensive to operate.

Beyond construction and transactions, the crisis is also reshaping the economics of operating existing real estate assets. Diesel prices in Nigeria have risen from approximately N1,300 per litre at the start of 2024 to N1,950 per litre today. For commercial and mixed-use assets dependent on alternative power, the impact is material. Facility managers are reporting sustained margin compression, with service charge commitments in many assets failing to keep pace with actual operating costs. For occupiers, the effective cost of occupation is rising independently of headline rent, altering affordability calculations across office, retail, and residential assets.

What does the market require now?

Developers with live off-plan commitments

The combination of a 20% construction cost increase and the return of phase-by-phase contractor pricing has broken the economics of fixed-price off-plan commitments made before December 2025. Developers managing this position must open renegotiation conversations immediately, with full cost transparency. Silence and specification downgrades carry higher long-term reputational costs than a transparent but commercially difficult renegotiation. New project launches should be structured on indexed, milestone-based pricing from the outset. Fixed-price assumptions that no contractor can credibly honour are increasingly being phased out in the current environment.

Investors and capital allocators

In volatile times, stability wins. Existing stabilised assets with verifiable operating cost and income profiles carry materially lower risk and are increasingly being preferred by investors compared to new development commitments. Ongoing off-plan projects that are experiencing cost-over-runs require independent verification of the developer's cost-to-complete, financing headroom, and contractor arrangements before any further capital is committed. For investors underwriting new acquisitions, operating cost assumptions derived from 2024 data are no longer reliable. The N1,950 per litre diesel price, if sustained, structurally reprices the operating economics of any asset dependent on alternative power. We expect to see those prices reflected in entry pricing decisions.

Operators and facilities managers

Occupiers faced with revised service charge invoices without prior communication or cost explanation typically respond adversarially. That, however, is changing. Tenants are becoming more receptive to discussing ways to mitigate the impact of the increases in the short term. In the medium to long term, a more structural fix will be shared energy infrastructure and alternative fuel arrangements.

If you are looking for more definitive and structured guidance on what to do; how to stay ahead of the market as a developer, buyer or facility manager, reach out to our advisory team - advisory@fortrenandcompany.com.

We love your feedback and look forward to hearing from you! Join the conversation on LinkedIn and Instagram and let us know what you think about the impact of the war on the market or your business.

With just 3,577square meters in land mass, Lagos is home to over 17 million residents, making it one of the most densely populated cities in the world. One of the most pronounced effects of clear overpopulation in overcrowded cities like Lagos is the increase in informal settlements, land grabbing, and illegal construction. Internal data from the Lagos State government shows that more than 349 buildings have been erected illegally and do not comply with the planning laws set out by the state. In response, the Lagos State Building Control Agency (LASBCA) and the Ministry of Physical Planning and Urban Development have intensified enforcement of planning laws to ensure that buildings within Lagos State are designed, constructed, and maintained to a high standard of safety. Their enforcement efforts have led to numerous building demolitions and are primarily targeted at three recurring violations across the state, which we will be discussing below.

- Lack of building development permit:

- sdfds

-

Failure to obtain required development permits remains one of the most common triggers for demolition across Lagos. Under Section 27(1) of the Lagos State Urban and Regional Planning and Development Law, no building is allowed to be erected across the state, except when necessary permits and approvals have been duly sought and obtained. “No person shall carry out any development in Lagos State without obtaining a permit from the relevant planning authority.” Non-compliance with section 27(1) of the Lagos State Urban and Regional Planning and Development Law authorises the state government to demolish any building that has not sought and obtained the necessary approvals. Despite this clear guideline, unauthorised construction continues to proliferate in the state. In a recent enforcement action, 13 illegal buildingswere demolished in Lagos for non-compliance, highlighting the Government’s resolve to clamp down on developments that violate planning regulations. Several factors may explain why some developers bypass the approval process, including a lack of awareness of regulatory requirements, the perceived complexity or delay in obtaining permits, and, in some cases, a calculated risk to evade official fees or oversight. While these issues don’t justify non-compliance, they underscore the need for continued public education, transparency, and reform of the permitting process.

- Encroachment on Drainage Channels and Setbacks:

Building on drainage channels and designated setbacks stands out as one of the leading causes of demolition across Lagos. This issue not only breaches planning regulations but has also contributed to environmental and public safety risks.The Lagos State Building Control Agency(LASBCA) mandates a minimum setback of nine (9) meters for residential buildings in high-density, flood-prone zonessuch as Victoria Island, Apapa, and the Lekki Peninsula Schemes I and II. Despite these regulations, many developers have reclaimed and erected structures directly on waterways, obstructing water flow and increasing the risk of flooding. Recently, the Lagos state government marked 39 buildingsfor demolition in the Eti-Osa Local Government Area (mostly along the Ikota corridor) for obstructing drainage channels and encroaching.Similar actions have been taken in other areas like Amuwo Odofin. These demolitions have left many homeowners devastated. In response, affected owners have petitioned the government through their community associations, while others seek court injunctions to challenge the demolition or delay it pending clarification of their land status. Urban experts, however, emphasise the need for property buyers to secure proper planning permits from the Lagos StatePhysical Planning Permit Authority(LASPPPA) before embarking on any building or development project within the state.In many cases, properties built on canals, drainage channels, or government-designated right-of-way have little to no legal standing, making it difficult for affected owners to obtain compensation or favourable rulings in court. This is because such developments typically contravene established planning laws and are considered public safety hazards. We love your feedback. Let us know what you think about this article or your experience renting in Africa by sending an email toadvisory@fortrenandcompany.com. You can also join the conversation here onLinkedIn.

.jpg)

.jpeg)